Over the past year or so, we have seen a rise in interest rates and fixed deposits have offered quite attractive returns. Some may be inclined to put all their savings into these guaranteed bank deposits, but is this a smart decision?

I have spoken to many in the past year that are putting off investing because they find fixed deposits more favourable. They believe (which is true) that investments, such as equity and property, is uncertain. So they would rather pick the safer option of fixed deposits. Whilst I do agree it is always a good idea to have liquid cash and sufficient savings, I do believe that your excess money is better off growing elsewhere.

Cash Cannot Beat Inflation

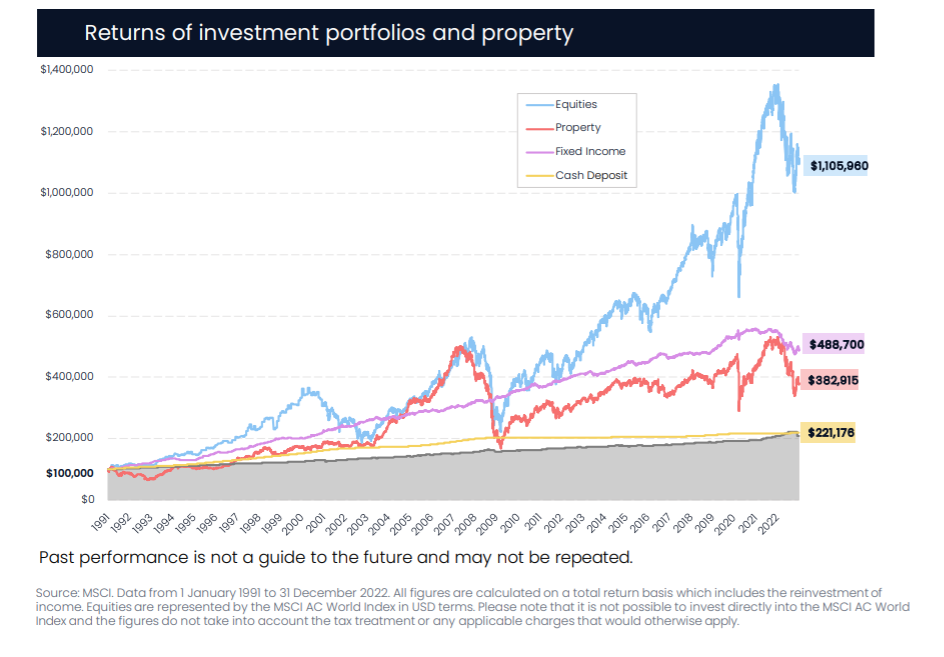

When you put your money in a fixed deposit, you will only gain the guaranteed amount, never any more. Whilst some see this as a good thing, in periods of high inflation (like over the past couple of years), your cash is losing spending power. And inflation is a problem that will always be there; it is not something we can ignore, and historically bank deposits have not battled inflation in comparison to equities.

Lock Ups & Opportunity Costs

In order to receive the guaranteed rate of return of a fixed deposit, you quite often will have to fulfil a tenure. I will admit that these days you can find fixed deposits with quite short tenures, but this often means that inflation may have eroded your guaranteed returns, leaving you with net zero or even negative gains! This also means that you are exposed to reinvestment risks; you as an investor may not be able to reinvest the cash you receive from a matured fixed deposit at the same or better rate again. This shows that bank deposits are good for short-term situations, but have more cons over the long-term. In contrast, historically, investing in equities or bonds have proven to grow capital and protect yourself from inflation.

‘Safe’ May Not Really Be Safe

It has become more apparent recently that the chance of a bank defaulting may not be is minute as we once thought- just look at Credit Suisse, Signature Bank and SVB to name a few. This means that your ‘guaranteed return’ may not actually be guaranteed. Banks are covered by the Deposit Protection Scheme, but take note that generally these limits are not very high. This means that if you have anything more in a fixed deposit, or indeed in a bank account, and the bank folds, they are only obligated to pay you up to that limit, nothing more. To avoid this, it may be a sensible idea to spread your cash across different institutions, not leaving all your assets with one bank. Investing in portfolios can also help you diversify risk, whilst having access to possible high returns, and holding up against inflation long-term.

If anything, market volatility has proven to us that a few key financial principles, such as planning long-term and diversifying to mitigate risk, are very important guidelines to follow. Whilst fixed deposits seem attractive short-term, they expose you to reinvestment risk, and are therefore only beneficial for short-term savings. Focusing all your financial planning on one bank or indeed one savings account, means that you are not diversifying, and not only are you at risk if the bank defaults, but you are also missing out on possible higher returns you could be getting from investment. Cash may be key for every-day living, but it is definitely not king when it comes to successful, long-term planning.