If you’ve been in Singapore the past few years, you’ve probably noticed two things: your grocery bill has gone up, and your mortgage repayments back at home might have too. Interest rates and inflation don’t just impact big economies – they hit everyday expats in very real ways.

The challenge? These two forces often work together to squeeze your finances from both ends. Inflation erodes your purchasing power, while higher interest rates increase the cost of borrowing. But with the right strategies, you can protect yourself, and even find opportunities.

1. How Interest Rates & Inflation Work Together

• Inflation: Prices rise, your money buys less. • Interest Rates: Central banks adjust rates to try to control inflation, which impacts loan costs and investment returns. • For Expats: You might be earning in SGD, paying loans in another currency, or vice versa…meaning you face multiple layers of impact.

2. Impact on Mortgages & Loans

• Floating Rate Loans: Your repayments can rise quickly as interest rates climb. • Fixed Rate Loans: Offer short-term protection but may revert to higher rates later. • Multi-Currency Loans: Add currency risk to the mix; a weakening home currency can make repayments more expensive.

If you’re planning to be in Singapore for several years, explore refinancing or partial prepayment to lock in manageable terms.

3. Investment Strategies in High Inflation

• Equities with Pricing Power: Companies that can pass increased costs to customers. • Inflation-Linked Bonds: Adjust payouts based on inflation rates. • Real Assets: Property, REITs, and infrastructure funds often provide inflation protection. • Shorter Duration Bonds: Less sensitive to rising rates than long-duration bonds.

4. Cash & Emergency Funds

• Keep enough liquidity for safety (3–6 months of expenses), but avoid holding excessive cash, as inflation will erode its value. • Consider short-term fixed deposits or money market funds for better returns without high risk.

5. Currency Management

If you’ll eventually move your money to another currency (for retirement or repatriation), inflation and interest rate differences between countries matter. • Diversify across currencies. • Use hedged share classes for global funds where appropriate.

6. SRS & Long-Term Planning

When rates rise, bond-heavy SRS portfolios may underperform. Consider: • Increasing equity exposure if suitable for your risk tolerance. • Adding assets less sensitive to rate hikes.

Interest rates and inflation don’t need to derail your financial plans. By actively managing your loans, investments, and currency exposure, you can turn economic headwinds into manageable breezes, and even use them to your advantage.

Singapore might be one of the most expensive cities in the world, but for many expats, the hidden cost isn’t just rent or coffee; it’s the slow erosion of your purchasing power. Inflation is a quiet thief. If you’re earning, saving, or investing in Singapore, you need a strategy that works now and in the future.

This guide will show you how to inflation-proof your portfolio without taking unnecessary risks, and without ignoring the fact that, as an expat, your financial life may span multiple currencies and countries.

1. Understand How Inflation Hits Expats in Singapore

For locals, inflation is mostly about cost of living. For expats, it’s a triple hit:

• Local inflation — price rises in SGD for housing, food, and services. • Imported inflation — the cost of goods from abroad. • Currency erosion — if your savings or income are tied to a weakening home currency.

Example: If you’re paid in SGD but plan to retire in GBP, you have to watch both Singapore’s inflation rate and the SGD-GBP exchange rate.

2. Diversify Across Asset Classes

No single investment will protect you perfectly, but a balanced mix can give you resilience.

• Equities: High-quality companies with pricing power can pass costs to customers. • Bonds: Shorter-duration bonds protect better in rising-rate environments; inflation-linked bonds adjust payouts in line with inflation. • Real Assets: Property (physical or REITs) and commodities can hedge against rising prices. • Alternative Investments: Infrastructure funds or private equity (if suitable for your profile).

3. Use Currency Hedging Wisely

Many expats ignore currency risk until it bites. Consider: • Hedged share classes of global funds. • Holding a mix of home-currency and SGD assets. • Using multi-currency accounts to park funds strategically.

4. Review Your SRS & Retirement Investments

SRS investments are in SGD, so if you plan to retire overseas, include an FX-diversification strategy. Inflation-proofing here might mean:

• Adding global equity funds. • Including a small allocation to commodities or infrastructure. • Avoiding locking into overly long fixed-income instruments when rates are rising.

5. Keep Cash — But Not Too Much

Cash is important for short-term stability, but inflation eats it fast. • Keep 3–6 months’ expenses in an easy-access account. • For surplus, use short-term fixed deposits or money market funds.

6. Regularly Rebalance

Inflationary periods can quickly skew your portfolio allocation. Make annual or semi-annual rebalancing a habit.

Inflation isn’t a storm to be waited out, it’s a tide you have to swim against. With the right asset mix, currency strategy, and regular reviews, your portfolio can not just survive but thrive in Singapore’s evolving economic climate.

As we approach the end of 2024, the global investment landscape has undergone significant changes influenced by a myriad of factors including economic recovery post-pandemic, geopolitical tensions, and advancements in technology. For expatriates, understanding these market conditions is crucial for making informed investment decisions. This article delves into the prevailing market trends, key considerations for expats, and strategic insights to navigate the investment landscape effectively.

Overview of Market Conditions

Global stock markets registered strong gains in Q1 amid a resilient US economy and ongoing enthusiasm around AI. Expectations of interest rate cuts also boosted shares although the pace of cuts is likely to be slower than that market had hoped for at the turn of the year. Bonds saw negative returns in the quarter.

Strength in some Asian markets helped emerging market equities outperform developed markets in Q2. Stocks related to the AI theme continued to perform strongly. The European Central Bank cut interest rates, but sticky inflation kept other major central banks on hold.

In Q3, global equities gained despite pronounced volatility on several occasions. Emerging markets performed strongly, supported by the announcement of new stimulus measures in China. Interest rate cuts in the quarter, and the prospect of more to come, helped fixed income markets to deliver solid returns.

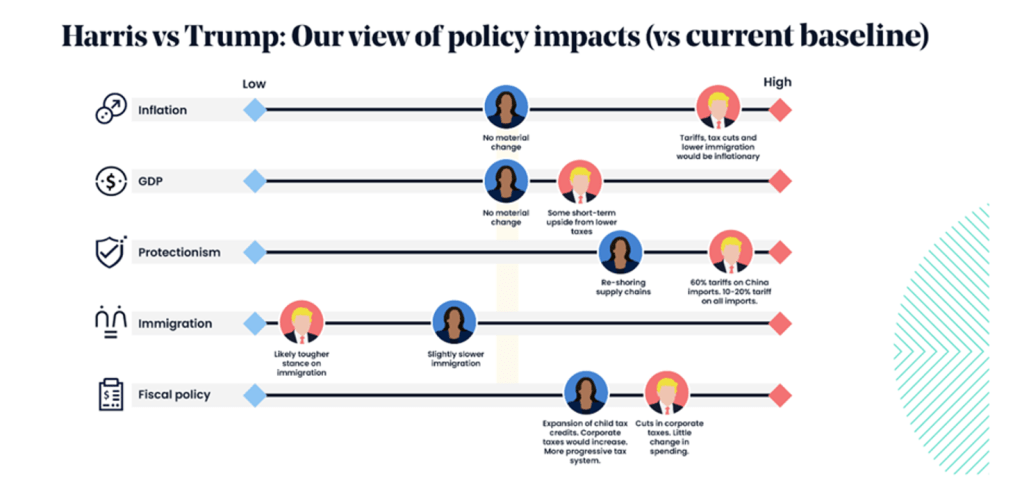

A Republican/Trump win will bring about a sea of changes, but this would not be immediate and not everything hoped for by the winning party would eventually be put into motion. Furthermore, history has shown that the outcome of elections does not affect the long-term trajectory of markets, therefore it remains paramount to have a broad and diversified portfolio and not lean excessively into any “Trump themes” that may or may not happen in the future.

History has shown it is unwise to make significant adjustments based on political events. Market volatility is often based on speculation and not any change to fundamentals.

At times of heightened uncertainty, it is important to remain faithful to our investment principles and process.

In Q1’24, markets rose as corporate earnings came in better than expected while AI optimism continued. A less hawkish than expected stance from central banks also boosted sentiment and the Fed affirmed rate cuts in 2024.

Q2’24 started off with a pullback on uncertainly over the rates outlook and stronger than expected economic data, but later rallied through the rest of Q2’24 as the disinflation trend came back on track and as the ECB started its rate cut cycle.

Markets gained in Jul’24 as optimism from the continued disinflationary trend in the U.S. reinforcing expectations of further rate cuts in H2’24.

Aug’24 started with a significant pullback as weaker than expected U.S. jobs and manufacturing data raised fears of a recession, while the unwinding of the carry trade exacerbatedvolatility. Losses were pared as recent economic data pointed to economic moderation rather than weakness, while the Fed confirmed a rate cut in Sep’24.

Sep’24, historically one of the weakest months in the calendar year, initially saw a pullback as worries over an economic slowdown appeared to weigh on sentiment. Markets later rebounded as investors looked forward to the first Fed rate cut, where the Fed cut rates by 50 bps and projected two more 25 bps cut in Nov’24 & Dec’24.

Reflecting on Trump’s previous presidency, high yield bonds & stocks outperformed due to favourable policies, which were pro-business and pro-markets.

Economic Recovery and Growth

The global economy has shown signs of recovery, with the International Monetary Fund (IMF) projecting a growth rate of around 3.5% for 2024. This recovery has been uneven across regions, with advanced economies experiencing slower growth compared to emerging markets. Countries in Asia, particularly India and Southeast Asia, have emerged as hotspots for investment due to their young demographics and increasing consumer spending.

Inflation and Interest Rates

Inflation remains a pressing concern, particularly in developed nations like the United States and the European Union. Central banks have responded by adjusting interest rates, with the Federal Reserve maintaining a cautious stance to balance growth and inflation. As of late 2024, interest rates are expected to stabilize, providing a more predictable environment for fixed-income investments.

Key Market Trends

Understanding the underlying trends is essential for expats looking to invest. Here are several key trends shaping the investment landscape:

Key Market Opportunities 2024/2025

We believe 2025 could be a year of relative clarity in global equity markets. The resolution of the US election and other key global elections has removed some critical policy question marks that had hampered investment, and pandemic-era shifts in supply chains have now solidified into a new post-Covid normal.

We expect a return to fundamentals in 2025, with the macro stories that dominated markets in 2024 giving way to a focus on companies’ individual strengths and weaknesses – this supports our ethos of global managers & active portfolio management.

In particular, the EM growth outlook is a relative bright spot in the global context, with disinflation, Chinese policy stimulus, and Fed rate cuts being supportive. Stock and currency market valuations remain undemanding.

Idiosyncratic trends within Emerging Markets imply scope of portfolio diversification too.

Fixed Income Outlook

During the third quarter, fixed income markets began to receive the policy rate cuts they had been craving for some time. Central banks had been reluctant to reduce rates too soon, as elements of inflation stickiness persisted across all major developed economies. This was particularly evident in the US and the UK, leading policymakers to maintain restrictive monetary policies. The European Central Bank was the first to cut rates, as Germany, the powerhouse of the European Union, continued to struggle with a range of economic headwinds. While some peripheral countries performed more strongly, this was overshadowed by ongoing concerns about the largest economy in Europe. The Bank of England followed with a modest 25-basis-point rate cut during the review period, despite pockets of inflationary pressure remaining in the UK economy. The Federal Reserve was the last major central bank to cut rates, announcing a 50-basis-point reduction at the end of September. This cut was larger than some commentators had expected and may have been designed to avoid any interference with the upcoming US Presidential election. Yield differentials between sovereign bonds and their investment-grade and high-yield credit counterparts remained relatively compressed. Investors continued to be confident that the economic backdrop was sufficiently supportive of corporate borrowers, making any major shift in the default landscape unlikely in the short to medium term. Supply was generally well received, and, in a departure from historical norms, new issues were often priced at a tighter yield differential than the existing debt of the same issuer.

Considerations for Expat Investors

Expat investors face unique challenges and opportunities. Here are key considerations to keep in mind when investing in the current market:

Currency Fluctuations

Currency risk is a significant factor for expatriates investing abroad. Fluctuations in exchange rates can impact the value of investments and returns. It is advisable for expats to consider currency-hedged investment options or diversify their portfolios across multiple currencies to mitigate this risk.

Tax Implications

Understanding the tax implications of investing in a foreign country is crucial. Tax treaties between countries can significantly influence the tax burden on expatriates. Engaging with a tax advisor familiar with international tax laws can help expatriates optimise their investment strategies and ensure compliance.

Regulatory Environment

Investment regulations vary significantly across countries. Expat investors should familiarise themselves with the legal and regulatory landscape of their host country, including any restrictions on foreign ownership of assets. Consulting with local financial advisors can provide valuable insights into navigating these regulations.

Strategic Investment Approaches

To successfully navigate the current investment market conditions, expatriates should consider the following strategic approaches:

Diversification

Diversification remains a cornerstone of a sound investment strategy. Expats should aim to diversify their portfolios across various asset classes, including equities, fixed income, real estate, and alternative investments. This approach can help mitigate risks associated with market volatility.

Focus on Long-Term Goals

While short-term market fluctuations can be tempting, expats should remain focused on their long-term investment goals. A long-term perspective can help investors weather temporary downturns and capitalise on the growth potential of their investments over time.

Continuous Education and Adaptation

The investment landscape is constantly evolving. Expats should prioritise continuous education regarding market trends, economic indicators, and emerging investment opportunities. Staying informed can empower investors to make proactive adjustments to their portfolios.

As we conclude 2024, the investment market is filled with both opportunities and challenges. Expats must approach this landscape with a well-informed strategy, taking into account the current economic conditions, market trends, and unique considerations related to their expatriate status. By staying informed and adaptable, expatriate investors can position themselves to navigate the complexities of the investment world and achieve their financial objectives.

We are all waiting on baited breath for the results of the US Election. What will the result mean for us as investors? Let’s take a look at a Macro Outlook overview & some key points to take note.

Macro Outlook

Attractive Valuations

• Asian Emerging markets are currently offering more attractive valuations compared to U.S. and other developed markets.

• These attractive valuations present a cost-effective entry point for investors seeking growth opportunities.

Declining Inflation and Interest Rates

• Recent trends indicate a decline in inflation rates across many emerging markets. This trend is expected to lead to lower interest rates over the next 18 months to two years.

• Lower interest rates can stimulate economic growth by making borrowing cheaper, which can boost consumer spending and corporate investment.

Weakening U.S. Dollar

• A weaker dollar can improve trading conditions for emerging market economies by making their exports more competitive on the global stage.

• A weaker dollar can attract foreign investment capital, as returns from these investments may be amplified when converted back into stronger currencies.

Bond Market Opportunities

• Yields continue to be elevated as compared to pre-2022, at the top of its percentile throughout history.

• With interest rates stabilising, fixed income, which exhibits 1/3 the volatility of equities, can act as a defensive portfolio diversifier, and an investor can lock in current yields at above average levels.

• With higher starting yields, expected forward returns are consequently higher and the correlation and statistical significance is high.

• In this Fed pause cycle, yields have fallen lesser than average, and a mean reversion would see a larger potential for capital appreciation.

What If Trump Wins?

I was going to include ‘What If Harris Wins?’…but it seems like that probably won’t be the case! So what happens if Trump does win?

•Trump’s policy around trade tariffs, tax & immigration would be inflationary.

•There would be less interest rate normalisation, as the Federal Reserve may not be able to cut interest rates as rapidly.

•Reflecting on Trump’s previous presidency, high yield bonds & stocks outperformed due to favourable policies, which were pro-business and pro-markets.

• During his last election, in November 2016, small caps in those initial months performed well, double the performance of the S&P 500.

Graph above shows Small Cap ETFs in 2016

Investment Opportunities

· Many emerging market assets have been undervalued in the past, providing a compelling entry point for investors. By reallocating funds into EM/Asia funds, we can capitalise on these undervalued opportunities, positioning ourselves for substantial growth as these markets normalise.

· In addition, high yield bonds are less sensitive to inflation and have a current distribution yield of 7.8%.

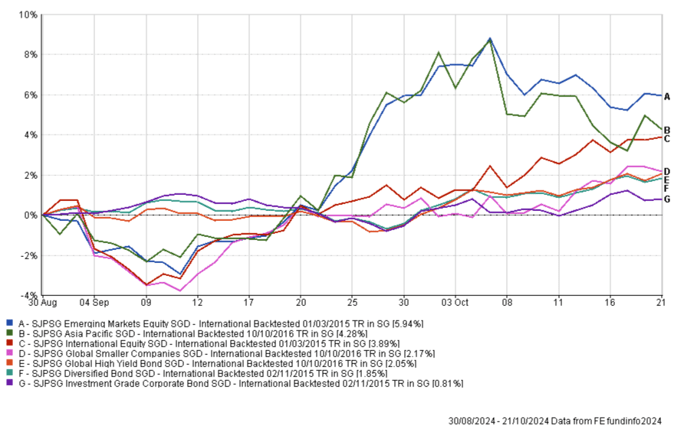

A Tale of Two Halves: After the Fed rate cut, we see an uptick & opportunity in Asia & EM. We also see a stable & resilient Global High Yield Bond.

Despite the doom and gloom you might hear in the news, the world economy is showing some grit, holding its own. This has given central banks a bit of wiggle room to tweak interest rates, which is good news for stocks, though not so much for gold. However, with the political scene being a tad unpredictable, gold remains a hot ticket item.

All That Glitters: Gold Market Buzz

The gold market is shifting gears. Its focus is moving from Chinese investment and central bank purchases towards anticipation of interest rate drops in Western economies. Gold prices are soaring, especially after the European Central Bank’s second rate cut. Traders in the futures market are hopeful, expecting lower interest rates, and the physical market is buzzing with investors seeking safer options.

However, history teaches us that interest rate cuts alone don’t guarantee a gold price surge. In the past, gold usually climbed only if rate cuts led to a recession, averaging a 15.5% increase within a year. If there was no recession post-cuts, gold prices typically fell by around 7%.

Stock Market Standouts

US stock markets have generally done well when the Federal Reserve cuts rates, especially if there’s no subsequent economic slump. Since the 1980s, the S&P 500 has averaged a 14.2% return in the year after initial cuts, outperforming the average return of 10.4% over the same period. This suggests that lower interest rates, without a corresponding recession, usually make for a good stock market environment.

While the economic backdrop looks positive, market ups and downs may persist due to uncertainties around the upcoming U.S. election and concerns of economic slowdown. However, these fluctuations might be a blip in a larger upward trend. So, long-term investors might want to keep their eye on U.S. large-cap growth stocks, which are likely to lead the charge in this bull market.

Emerging Markets: A Mixed Bag

Historically, when the Fed cuts rates, emerging market (EM) stocks tend to do well, especially if there’s no recession. However, the U.S. elections could sway the outlook for EM assets. Any protectionist policies could hit them hard. So, given the current uncertainties, it might be wise to hold off on heavy EM investment until the economic picture becomes clearer.

Data shows that after the first rate cut, EM stocks often outdo developed markets, especially if a recession is avoided. While initial performance might not show big differences, a clearer picture usually emerges about a quarter later as investors assess the economic landscape.

While EM stocks might not be a priority right now, EM bonds could offer good returns in this period, presenting potential investment opportunities amid U.S. growth concerns. Things might become clearer once election risks reduce and signs of economic stability appear.

The Fed & its Rate Cut

The Federal Reserve cut interest rates by half a percentage point, the first reduction since early in the Covid pandemic, to prevent a slowdown in the labor market. Rates now range from 4.75% to 5%, impacting short-term borrowing costs for banks and consumer products like mortgages and loans. The committee plans further cuts, aiming for another full percentage point by the end of 2025 and a half point in 2026, despite a dissenting vote from Governor Michelle Bowman.

The cut seeks to restore price stability without increasing unemployment, which remains low at 4.2%. Although job gains have slowed and the unemployment rate is expected to rise to 4.4%, inflation outlook has improved to 2.3%. The decision caused market volatility, with the Dow Jones fluctuating significantly.

Concerns persist about the labor market, as hiring rates have dropped, suggesting potential future rate cuts may vary among committee members. The Fed’s last rate reduction was in March 2020, followed by three increases due to inflation. While other central banks are cutting rates, the Fed continues to reduce its bond holdings, lowering its balance sheet to $7.2 trillion, down $1.7 trillion from its peak.

Investor Takeaway

Overall, the current environment looks good for stocks, though the U.S. presidential election could cause some market nerves. For gold, while the environment usually doesn’t favor price increases, it still holds an important place as a diversifier in uncertain times. As central banks tweak their strategies, investors should feel comfortable with the current rate cuts, while remembering that every cycle is unique, especially in our current politically charged world.

Over the past year or so, we have seen a rise in interest rates and fixed deposits have offered quite attractive returns. Some may be inclined to put all their savings into these guaranteed bank deposits, but is this a smart decision?

I have spoken to many in the past year that are putting off investing because they find fixed deposits more favourable. They believe (which is true) that investments, such as equity and property, is uncertain. So they would rather pick the safer option of fixed deposits. Whilst I do agree it is always a good idea to have liquid cash and sufficient savings, I do believe that your excess money is better off growing elsewhere.

Cash Cannot Beat Inflation

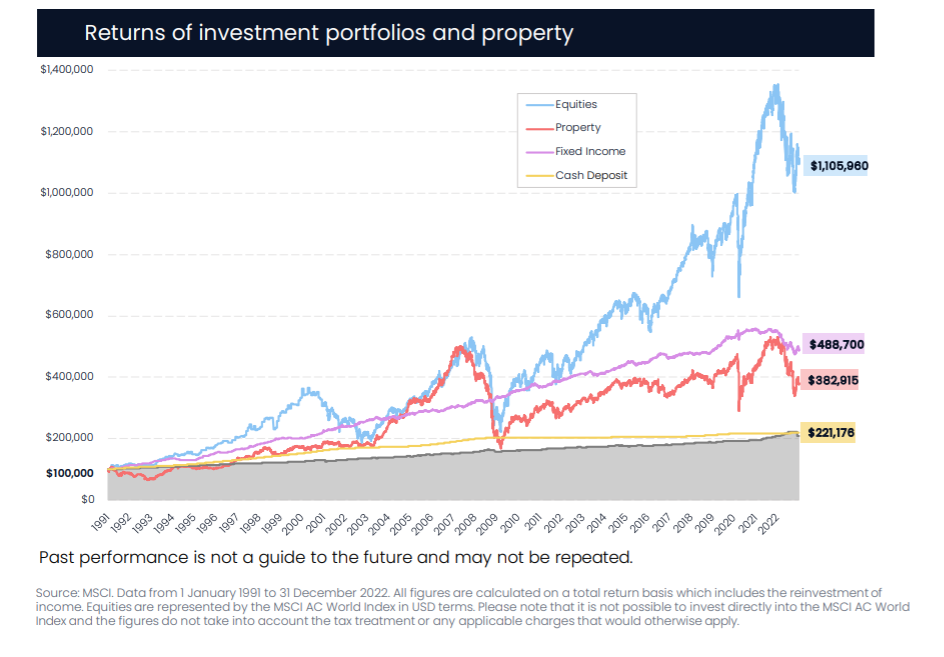

When you put your money in a fixed deposit, you will only gain the guaranteed amount, never any more. Whilst some see this as a good thing, in periods of high inflation (like over the past couple of years), your cash is losing spending power. And inflation is a problem that will always be there; it is not something we can ignore, and historically bank deposits have not battled inflation in comparison to equities.

Lock Ups & Opportunity Costs

In order to receive the guaranteed rate of return of a fixed deposit, you quite often will have to fulfil a tenure. I will admit that these days you can find fixed deposits with quite short tenures, but this often means that inflation may have eroded your guaranteed returns, leaving you with net zero or even negative gains! This also means that you are exposed to reinvestment risks; you as an investor may not be able to reinvest the cash you receive from a matured fixed deposit at the same or better rate again. This shows that bank deposits are good for short-term situations, but have more cons over the long-term. In contrast, historically, investing in equities or bonds have proven to grow capital and protect yourself from inflation.

‘Safe’ May Not Really Be Safe

It has become more apparent recently that the chance of a bank defaulting may not be is minute as we once thought- just look at Credit Suisse, Signature Bank and SVB to name a few. This means that your ‘guaranteed return’ may not actually be guaranteed. Banks are covered by the Deposit Protection Scheme, but take note that generally these limits are not very high. This means that if you have anything more in a fixed deposit, or indeed in a bank account, and the bank folds, they are only obligated to pay you up to that limit, nothing more. To avoid this, it may be a sensible idea to spread your cash across different institutions, not leaving all your assets with one bank. Investing in portfolios can also help you diversify risk, whilst having access to possible high returns, and holding up against inflation long-term.

If anything, market volatility has proven to us that a few key financial principles, such as planning long-term and diversifying to mitigate risk, are very important guidelines to follow. Whilst fixed deposits seem attractive short-term, they expose you to reinvestment risk, and are therefore only beneficial for short-term savings. Focusing all your financial planning on one bank or indeed one savings account, means that you are not diversifying, and not only are you at risk if the bank defaults, but you are also missing out on possible higher returns you could be getting from investment. Cash may be key for every-day living, but it is definitely not king when it comes to successful, long-term planning.

We’re all been hearing about how bad inflation is and that it’s increasing etc. But what does this actually mean and how does it have a lasting affect on our money planning?

What Is Inflation?

Simply put, inflation is when the cost of goods and living increases. Whilst some see this as a bad thing, slight inflation is good as it is a sign of a growing economy; meaning more employment, higher profits and an increase in production. But, right now, we are seeing a significant rise in inflation. In December of 2021, Singapore saw inflation hit a 9 year high of 4%.

How It Affects Us Now

This increase directly affects us, and you may have even felt a bit of a pinch. Food is a bit more expenses and energy prices seem to have gone through the roof. All of this means that your cold hard-earned cash has less spending power, essentially meaning that you cannot buy as many things with the same amount of money as you used to. What further exacerbates this problem is bank interest rates; most current accounts in Singapore have an annual interest rate of 0.05%, meaning the bank gives you that much extra each year (not a lot at all). If current inflation rate is at 4%, you are losing 3.95% of your money every year by just leaving it in your bank account! This means that whilst you are earning money, not only are things getting more expensive but you’re losing money in your bank account too!

How It Affects Our Future

As you can imagine, this situation has a massive knock-on effect for our futures. If inflation increases, or even plateaus at say about 2%, you are still losing money in your bank account. Food, housing, medicine and energy will continue to go up in price, meaning each year you will either be able to afford less, or have to spend more to keep up. Not only that, your savings will not be as powerful as it once was…so you can see how this is a problem two-fold!

How Can We Stop This?

But fear not! If we prepare now ahead of time, we can manage inflation so that it doesn’t eat away at our savings. There are a few things you can do in preparation: first, include inflation in any planning you do. Want to save up for a holiday in 5 years’ time? Inflate your ticket and hotel prices by at least 2% per annum (3% if you want to be safe). Secondly, consider using vehicles and instruments that will offer you higher returns than your current bank account- any % higher than current inflation rate will give you a positive yield, and will ensure that your savings don’t run dry. I also think it’s best to create multiple avenues for growing your money, so that if one option is not doing well, at least you have money in different areas that you can withdraw from. Lastly, do not underestimate how much different sectors will increase. Food, healthcare, housing etc. do not always follow the same trend or inflation rate. Ensure you have medical expenses covered and calculated into your long-term planning, as well as remembering that your income will not go as far in future unless you ensure there are increases.

Essentially, it is best to start planning now instead of panicking later on in life, realising that you could have prepared for inflation but didn’t. As always, it’s best to stay in-the-know, and consult a professional when it comes to your financial planning.