As we approach the end of 2024, the global investment landscape has undergone significant changes influenced by a myriad of factors including economic recovery post-pandemic, geopolitical tensions, and advancements in technology. For expatriates, understanding these market conditions is crucial for making informed investment decisions. This article delves into the prevailing market trends, key considerations for expats, and strategic insights to navigate the investment landscape effectively.

Overview of Market Conditions

Global stock markets registered strong gains in Q1 amid a resilient US economy and ongoing enthusiasm around AI. Expectations of interest rate cuts also boosted shares although the pace of cuts is likely to be slower than that market had hoped for at the turn of the year. Bonds saw negative returns in the quarter.

Strength in some Asian markets helped emerging market equities outperform developed markets in Q2. Stocks related to the AI theme continued to perform strongly. The European Central Bank cut interest rates, but sticky inflation kept other major central banks on hold.

In Q3, global equities gained despite pronounced volatility on several occasions. Emerging markets performed strongly, supported by the announcement of new stimulus measures in China. Interest rate cuts in the quarter, and the prospect of more to come, helped fixed income markets to deliver solid returns.

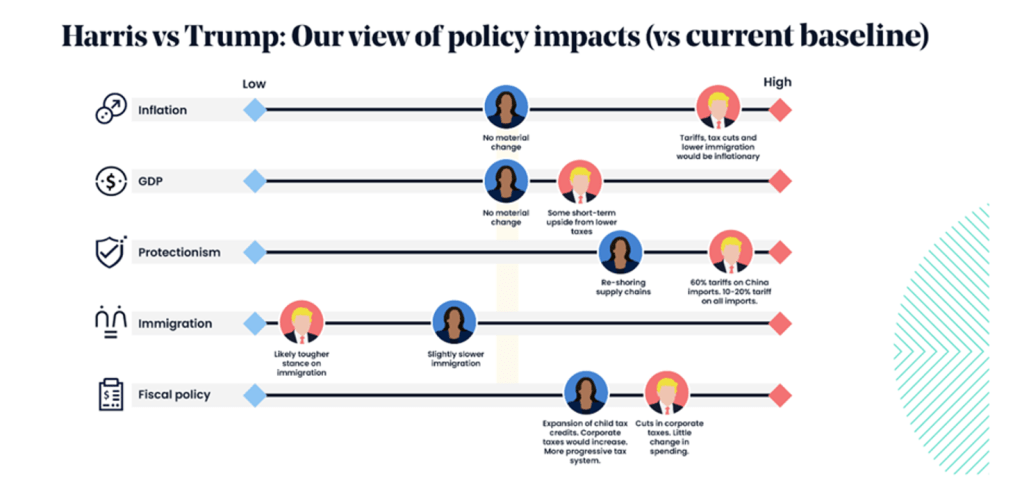

A Republican/Trump win will bring about a sea of changes, but this would not be immediate and not everything hoped for by the winning party would eventually be put into motion. Furthermore, history has shown that the outcome of elections does not affect the long-term trajectory of markets, therefore it remains paramount to have a broad and diversified portfolio and not lean excessively into any “Trump themes” that may or may not happen in the future.

History has shown it is unwise to make significant adjustments based on political events. Market volatility is often based on speculation and not any change to fundamentals.

At times of heightened uncertainty, it is important to remain faithful to our investment principles and process.

- In Q1’24, markets rose as corporate earnings came in better than expected while AI optimism continued. A less hawkish than expected stance from central banks also boosted sentiment and the Fed affirmed rate cuts in 2024.

- Q2’24 started off with a pullback on uncertainly over the rates outlook and stronger than expected economic data, but later rallied through the rest of Q2’24 as the disinflation trend came back on track and as the ECB started its rate cut cycle.

- Markets gained in Jul’24 as optimism from the continued disinflationary trend in the U.S. reinforcing expectations of further rate cuts in H2’24.

- Aug’24 started with a significant pullback as weaker than expected U.S. jobs and manufacturing data raised fears of a recession, while the unwinding of the carry trade exacerbatedvolatility. Losses were pared as recent economic data pointed to economic moderation rather than weakness, while the Fed confirmed a rate cut in Sep’24.

- Sep’24, historically one of the weakest months in the calendar year, initially saw a pullback as worries over an economic slowdown appeared to weigh on sentiment. Markets later rebounded as investors looked forward to the first Fed rate cut, where the Fed cut rates by 50 bps and projected two more 25 bps cut in Nov’24 & Dec’24.

- Reflecting on Trump’s previous presidency, high yield bonds & stocks outperformed due to favourable policies, which were pro-business and pro-markets.

Economic Recovery and Growth

The global economy has shown signs of recovery, with the International Monetary Fund (IMF) projecting a growth rate of around 3.5% for 2024. This recovery has been uneven across regions, with advanced economies experiencing slower growth compared to emerging markets. Countries in Asia, particularly India and Southeast Asia, have emerged as hotspots for investment due to their young demographics and increasing consumer spending.

Inflation and Interest Rates

Inflation remains a pressing concern, particularly in developed nations like the United States and the European Union. Central banks have responded by adjusting interest rates, with the Federal Reserve maintaining a cautious stance to balance growth and inflation. As of late 2024, interest rates are expected to stabilize, providing a more predictable environment for fixed-income investments.

Key Market Trends

Understanding the underlying trends is essential for expats looking to invest. Here are several key trends shaping the investment landscape:

Key Market Opportunities 2024/2025

- We believe 2025 could be a year of relative clarity in global equity markets. The resolution of the US election and other key global elections has removed some critical policy question marks that had hampered investment, and pandemic-era shifts in supply chains have now solidified into a new post-Covid normal.

- We expect a return to fundamentals in 2025, with the macro stories that dominated markets in 2024 giving way to a focus on companies’ individual strengths and weaknesses – this supports our ethos of global managers & active portfolio management.

- In particular, the EM growth outlook is a relative bright spot in the global context, with disinflation, Chinese policy stimulus, and Fed rate cuts being supportive. Stock and currency market valuations remain undemanding.

- Idiosyncratic trends within Emerging Markets imply scope of portfolio diversification too.

Fixed Income Outlook

During the third quarter, fixed income markets began to receive the policy rate cuts they had been craving for some time. Central banks had been reluctant to reduce rates too soon, as elements of inflation stickiness persisted across all major developed economies. This was particularly evident in the US and the UK, leading policymakers to maintain restrictive monetary policies. The European Central Bank was the first to cut rates, as Germany, the powerhouse of the European Union, continued to struggle with a range of economic headwinds. While some peripheral countries performed more strongly, this was overshadowed by ongoing concerns about the largest economy in Europe. The Bank of England followed with a modest 25-basis-point rate cut during the review period, despite pockets of inflationary pressure remaining in the UK economy. The Federal Reserve was the last major central bank to cut rates, announcing a 50-basis-point reduction at the end of September. This cut was larger than some commentators had expected and may have been designed to avoid any interference with the upcoming US Presidential election.

Yield differentials between sovereign bonds and their investment-grade and high-yield credit counterparts remained relatively compressed. Investors continued to be confident that the economic backdrop was sufficiently supportive of corporate borrowers, making any major shift in the default landscape unlikely in the short to medium term. Supply was generally well received, and, in a departure from historical norms, new issues were often priced at a tighter yield differential than the existing debt of the same issuer.

Considerations for Expat Investors

Expat investors face unique challenges and opportunities. Here are key considerations to keep in mind when investing in the current market:

Currency Fluctuations

Currency risk is a significant factor for expatriates investing abroad. Fluctuations in exchange rates can impact the value of investments and returns. It is advisable for expats to consider currency-hedged investment options or diversify their portfolios across multiple currencies to mitigate this risk.

Tax Implications

Understanding the tax implications of investing in a foreign country is crucial. Tax treaties between countries can significantly influence the tax burden on expatriates. Engaging with a tax advisor familiar with international tax laws can help expatriates optimise their investment strategies and ensure compliance.

Regulatory Environment

Investment regulations vary significantly across countries. Expat investors should familiarise themselves with the legal and regulatory landscape of their host country, including any restrictions on foreign ownership of assets. Consulting with local financial advisors can provide valuable insights into navigating these regulations.

Strategic Investment Approaches

To successfully navigate the current investment market conditions, expatriates should consider the following strategic approaches:

Diversification

Diversification remains a cornerstone of a sound investment strategy. Expats should aim to diversify their portfolios across various asset classes, including equities, fixed income, real estate, and alternative investments. This approach can help mitigate risks associated with market volatility.

Focus on Long-Term Goals

While short-term market fluctuations can be tempting, expats should remain focused on their long-term investment goals. A long-term perspective can help investors weather temporary downturns and capitalise on the growth potential of their investments over time.

Continuous Education and Adaptation

The investment landscape is constantly evolving. Expats should prioritise continuous education regarding market trends, economic indicators, and emerging investment opportunities. Staying informed can empower investors to make proactive adjustments to their portfolios.

As we conclude 2024, the investment market is filled with both opportunities and challenges. Expats must approach this landscape with a well-informed strategy, taking into account the current economic conditions, market trends, and unique considerations related to their expatriate status. By staying informed and adaptable, expatriate investors can position themselves to navigate the complexities of the investment world and achieve their financial objectives.