Towards the end of 2023, I had the honour of speaking at the Fixed Income Leaders Summit in Singapore.

I also shared my thoughts on the bond market and how investors can handle market volatility.

Check out the video and write up here:

Towards the end of 2023, I had the honour of speaking at the Fixed Income Leaders Summit in Singapore.

I also shared my thoughts on the bond market and how investors can handle market volatility.

Check out the video and write up here:

Only one week after I posted about all the elections in 2024 and what this could mean for global geopolitics, Taiwan has elected Dr William Lai as their president.

This may make things difficult, as Lai has vowed to protect Taiwan from China’s aggression. Xi Jinping has labelled Lai as a troublemaker and obviously would not want Lai to threaten his One China policy. Moreover, tensions have risen after the US congratulated Taiwan on the result- something that China claims goes against the US’s unofficial relationship with Taiwan.

Washington also used phrases like ‘diplomacy’, ‘partnership’ and ‘shared interest and values’, which has of course annoyed Beijing even more. The relationship between Lai and Xi Jinping is so bad that William Lai is not allowed to travel to Mainland China or Hong Kong! The two have not been in communication since 2016. Will this mean that China will increase its economic pressure on Taiwan? Will they threaten military force like they did in 2022? Whatever will happen, it’s clear that tensions will surely rise, as Lai is pro Taiwanese independence.

Of course, the result of the US election will greatly affect China and Taiwan, also, so we will monitor closely as the situation unfolds.

2024 may be the biggest election year ever, with almost half of the globe voting! At least 64 countries, plus the European Union will be voting and holding national elections. This is a massive year for global politics, so I thought I would discuss some of the notable elections and ones that interest me (don’t worry, I shan’t talk about all 64!).

US

This one probably makes us groan, and I’m sure we’re all bored of hearing about Trump & Biden, but this is arguably the most important election out of the lot. The US is the largest global power, and this election could see a change in USA’s relationship with North Korea, China, Russia and their stance on the ongoing conflicts in Gaza and Ukraine, depending on who wins. Also this is probably the only one where one of the candidates was a previous president who got impeached twice?

Taiwan

I feel like the whole world has been holding their breath when it comes to Taiwan & China, and this election will be no different! The winner of the Taiwanese election will have a tricky balancing act with China, and it’ll be interesting to see if Beijing continues its hold on the island, and whether the imminent threat of invasion will remain.

North Korea

This is interesting, because I didn’t even know the Democratic People’s Republic of Korea had elections (?!). I’m sure the Kim family, who are seen as somewhat deities in North Korea, don’t have an opposition party? What’s even more interesting, is that every election has been given a ‘freedom & fairness’ score (with 0.00 not being free nor fair at all, with 1 being the most free and fair), and North Korea scored higher than a lot of countries! I thought it would score 0.00, but it scored 0.14, which was higher than Venezuela- which I also expected to be low! Countries that scored 0.00 were Syria, Mali, Chad and South Sudan.

India

This election will be one to watch; not only is this election the largest in the world, but India is a rising global power and one of the most populous countries on the globe. The outcome may change not only domestic policies, but also regional politics, particularly concerning China. It may also escalate (or hopefully deescalate) the country’s rising Muslim/Hindu tensions.

Russia

Shockingly another country that’s free & fairness is not at the bottom of the list (although it is above North Korea)! But I don’t think anyone will be shocked when Putin is re-elected and the current trajectory of Russia’s geopolitics continues- i.e. the war continuing.

EU

Sadly, we’ve seen a surge in right wing parties in Europe, and I’m wondering if this will continue into 2024? It seems that a lot of centre-right parties will maintain their current positions, with even far-right parties gaining traction. The main points for discussion will of course be how the EU navigates conflicts, such as in Ukraine and Gaza, along with its green policies and the EU budget. Deficit Rules were suspended during the pandemic, meaning that members were allowed to borrow whatever they wanted to support their citizens, but this is set to be scrapped in 2024, with Deficit Rules being reinstated. Will this create tension between members?

Indonesia

I don’t have a tonne of opinions on this, but I thought it was interesting to note that Indonesia’s elections are only being held over one day! That’s the largest single-day vote, and I wonder how they are going to pull that off in such a large country that has some very remote locations.

Ukraine

Even though Ukraine is under Martial Law, which normally prohibits elections, there has been talk of these elections continuing, as a mark of democratic health. However, this may prove to be too challenging to organise during a war, with safety being a main concern. Either way, Zelenskiy is set to run for a third term, and he will probably win, with his ratings still remaining very high. However, parliament would have to change the law so that Ukrainiens can vote from overseas.

UK

The outlook of British politics has been bleak for a while now, and with the Conservative Party being in power for the past 14 years, some believe that Labour will win the next election, which Sunak has said will be held this year. This is conflicting for me- whilst I am desperate to see the Conservative Party go, and end their reign of austerity, I’m not convinced that the Labour Party will do a better job. Not only that, I have found myself shocked at every vote and election result in the UK for the longest time. None of us thought Brexit would happen, and how naïve we were to think that we would remain. So I’ve learnt to never think that the obvious flaws of the current party, means that they won’t be re-elected!

Whilst this may be the biggest election year ever, it may also be the most challenging for democracy, with many elections being carried out unfairly, or with risk of danger. Not only that, shock decisions and outcomes may shake the geopolitical framework as we know it. It’s going to be an interesting year for sure.

For the full information on the freedom & fairness score, check out Our World In Data: https://ourworldindata.org/grapher/free-and-fair-elections-index and for the full list of elections, along with dates & scores, check out this great article by Time: https://time.com/6550920/world-elections-2024/.

Over the past year or so, we have seen a rise in interest rates and fixed deposits have offered quite attractive returns. Some may be inclined to put all their savings into these guaranteed bank deposits, but is this a smart decision?

I have spoken to many in the past year that are putting off investing because they find fixed deposits more favourable. They believe (which is true) that investments, such as equity and property, is uncertain. So they would rather pick the safer option of fixed deposits. Whilst I do agree it is always a good idea to have liquid cash and sufficient savings, I do believe that your excess money is better off growing elsewhere.

Cash Cannot Beat Inflation

When you put your money in a fixed deposit, you will only gain the guaranteed amount, never any more. Whilst some see this as a good thing, in periods of high inflation (like over the past couple of years), your cash is losing spending power. And inflation is a problem that will always be there; it is not something we can ignore, and historically bank deposits have not battled inflation in comparison to equities.

Lock Ups & Opportunity Costs

In order to receive the guaranteed rate of return of a fixed deposit, you quite often will have to fulfil a tenure. I will admit that these days you can find fixed deposits with quite short tenures, but this often means that inflation may have eroded your guaranteed returns, leaving you with net zero or even negative gains! This also means that you are exposed to reinvestment risks; you as an investor may not be able to reinvest the cash you receive from a matured fixed deposit at the same or better rate again. This shows that bank deposits are good for short-term situations, but have more cons over the long-term. In contrast, historically, investing in equities or bonds have proven to grow capital and protect yourself from inflation.

‘Safe’ May Not Really Be Safe

It has become more apparent recently that the chance of a bank defaulting may not be is minute as we once thought- just look at Credit Suisse, Signature Bank and SVB to name a few. This means that your ‘guaranteed return’ may not actually be guaranteed. Banks are covered by the Deposit Protection Scheme, but take note that generally these limits are not very high. This means that if you have anything more in a fixed deposit, or indeed in a bank account, and the bank folds, they are only obligated to pay you up to that limit, nothing more. To avoid this, it may be a sensible idea to spread your cash across different institutions, not leaving all your assets with one bank. Investing in portfolios can also help you diversify risk, whilst having access to possible high returns, and holding up against inflation long-term.

If anything, market volatility has proven to us that a few key financial principles, such as planning long-term and diversifying to mitigate risk, are very important guidelines to follow. Whilst fixed deposits seem attractive short-term, they expose you to reinvestment risk, and are therefore only beneficial for short-term savings. Focusing all your financial planning on one bank or indeed one savings account, means that you are not diversifying, and not only are you at risk if the bank defaults, but you are also missing out on possible higher returns you could be getting from investment. Cash may be key for every-day living, but it is definitely not king when it comes to successful, long-term planning.

Whilst I am a big advocate for looking forward, I have learnt over the past year that reflection is just as important. So, I thought that it would be beneficial to look back over the past year and think about all the challenges and accomplishments I have experienced.

Personal Challenges

I’m not going to dwell too much on this topic but I feel that it’s important to highlight because I have not had a perfect year- whilst my professional life has been a success story, I have had my own crosses to bear in my personal life. I recently lost someone very close to me, only a few weeks before Christmas, and this has made me remember even more that family is most important and we should cherish these moments that we have.

Many people have commented that I seem fine on social media and that I’m still going to work, so I must be ok, but this is truly not the case. Grief hits people differently, and I’m choosing to try to continue with the day to day.

Business Challenges

Of course, like the market, work life also has its ups and downs. Not only have we all struggled with the cost of living and the markets not recovering like we had hoped, but here in Singapore the job market has become extremely volatile. I’ve had lots of clients, and indeed friends, leave Singapore due to losing their jobs or finding better opportunities elsewhere. Luckily, I am still in contact with many and some have even returned to Singapore, but it just shows that nothing is certain, not even our jobs, which is why it is so important to plan, have emergency savings etc.

On top of this, as many may know, during the first half of the year I was feeling quite deflated about my work situation; I felt that I was frequently made to choose between work and my personal time, and I felt that I was neglecting other parts of me. If you have read my reflection post when I turned 30, I think you will understand a bit more. I was starting to feel like there was a glass ceiling too; the holistic planning I was providing for my clients had gaps in, as I could only provide certain solutions. This made me feel like there must be something more, something better, so that I can be offering my clients the best service possible.

Business Successes

This actually led me onto many business successes. I truly believe that if there’s something wrong in your life that you can make an effort to change, you should do so. So that’s what I did. When I turned 30 I changed my mindset, sorted out my work-life balance, upgraded my skills and even changed jobs. Now I can provide my clients with even more support and advice that before, with solutions that are more suited to the expat transience we so frequently see in Singapore. Not only that, the level of support and resources that I am receiving now means that I can have a wider reach; I’ve recently had amazing opportunities such as speaking at conferences, hosting my own launch event, attending investment insight conferences and as of next year I will hopefully be joining an advisory board (more news to come)!

Of course I need to thank of all those that entrusted me with these opportunities to speak and share my knowledge, but this has also proven to myself that I can do it- that lul in the middle of the year was only temporary, and I am very excited for the upward trajectory I appear to be on for 2024. I’ve managed to empower and inspire others through my articles, videos and podcasts, and I can feel like I’m really making a difference.

Personal Successes

I feel like this positivity and new lease of life when changing jobs has created a domino effect, where things in my personal life have also been going well. I’m a lot happier and less stressed, which means that I am able to nurture and spend time working on my relationships. My friendships have grown stronger this year, I have travelled for some beautiful weddings, and I’m very blessed that my friends shared their special days with me, and I will be travelling home for Christmas to spend some quality time with my family.

Whilst this year has been far from perfect, I’m very lucky to have the life I have- I have wonderful friends, family and husband, my career is on the up, and whilst there has been a lot of sadness too, I’m ready to grieve and put the effort into healing.

I hope you took something away from this and it wasn’t just a self-indulgent exercise; I encourage everyone to reflect during this time of year and look forward to the year ahead!

I’ve just finished my new ebook: Let’s Talk About Finance Basics For Young Women!

In this ebook, I’ll be delving into the socio and psychological consequences of financial literacy, along with how our upbringing could have affected our money mind. Not only that, I have a few strategies on how to discuss money without shame or judgement, along with some basic budgeting tips and what we should be saving for.

Feel free to read, share and let me know what you think!

I’m really happy to announce that I have started a new podcast on Spotify! I noticed that talking about money, especially as a woman, is still seen as a bit of a taboo subject. I’m here to empower and impart my knowledge for other expats in Singapore, on how to successfully navigate personal finances.

Click on the link below to listen- I release new episodes every Monday so be sure to tune in!

“People don’t turn down money! It’s what separates us from the animals.” – Jerry

Seinfeld is one of my all-time-favourite TV shows. Most people were into F.R.I.E.N.D.S (not that there’s anything wrong with that), but I much preferred the self-deprecating jokes of Jerry, George (especially George), Elaine, Kramer, and even Newman (hello, Newman). If you’re unaware of the plot of the show, it’s a show about nothing- four friends living in New York, navigating their tragic love and work lives. But what I never understood is how Jerry, an a comedian working the club circuit, and Kramer, who is perpetually unemployed, could afford to live in Manhattan. Like my Sex & The City and Homer Simpson article, let’s explore that here.

“Who goes on vacation without a job? What do you need a break from getting up at eleven?” – Jerry

Let’s start by talking about Jerry. Whist Seinfeld in real life is a mega multi-millionaire, that’s not the case in the show. In the show, Jerry is a lesser known comedian- and in the 90s comedians couldn’t supplement their income as much as they do now with social media posts and advertising. The New York Times did a study and found that the income range for comedians varied from about $30,000 per year, up to $200,000 a year. Jerry would have been on the lower end of this spectrum, earning about $35,000 per year, Market Watch estimates. This is fairly low, considering that Jerry’s apartment, 129 West 81st Street, is very close to Central Park, and is thus a prime location. Right now, a one-bedroom apartment in that area costs $3,000 a month. If we work backwards inflation-wise, back in the 90s that would have been about $1,200 a month. This would mean that, after tax, deductions and rent, Jerry would have $14,271 surplus income annually.

“Jerry, just remember, it’s not a lie if you believe it.” – George

If you watch the show, Jerry’s lifestyle is not that frivolous, unlike Carrie Bradshaw. And we know that Jerry has the ability to save as in one episode he buys his dad a Cadillac, which back then would have been more than $30,000. Speaking of cars, Jerry also had his own car, which, considering he lived in central New York, is a big expense. He could have just used public transport like the Subway, as parking in NY is expensive. Jerry drove a BMW, which would have cost about $40,000 back then. So how did he manage to pay for two cars amounting to about $75,000 in total with only a $1,189.25 monthly budget?!

“I’m disturbed, I’m depressed, I’m inadequate. I’ve got it all!” – George

So, Jerry’s lifestyle is not too difficult to comprehend; most of his money goes on rent and his car and he doesn’t do too much else. He mostly eats at home or at that very cheap café and is generally a good saver. But what does baffle me is Kramer- Cosmo is either unemployed, is in the process of suing someone, or is running one of his various get-rich-quick schemes. He is Jerry’s neighbour, so how could he afford it?!

“Do you have any idea how much time I waste in this apartment?” – Kramer

Kramer has almost had as many random jobs as Homer Simpson; Santa at a department store (which he got fired from for being a communist), a coffee table book author, a guy in police line-ups, the list goes on! All of these seem to not pay that much in terms of salary, and he turns down a lot of pay-outs from his lawsuits in exchange for things like free coffee or a billboard in Times Square. Why would Kramer pass up on so much cash if he has no stable income? This leads me to think…does he come from generational wealth?

“I’m speechless. I’m without speech.” – Elaine

I think the only valid conclusion I can come to is that Kramer’s father or his side of the family has left Kramer a lot of money. His mom works in a restaurant, so it’s probably not coming from her, but we don’t really hear anything about Kramer’s dad. Therefore, the only suitable answer I have is that Kramer’s dad is so rich that Kramer doesn’t care about money and can afford a decent apartment in central Manhattan and doesn’t need a job.

“You got a question? You ask the 8-ball.”- David Puddy

I will continue to review these shows that defy the laws of finance and budgeting, like Seinfeld, Sex and the City, and The Simpsons, but let’s not forget that the writers are very clever in smoothing out these questions by writing in things such as a rental cap, random relative’s inheritance or someone lending them money. But I do think it is funny how most of these shows are in the 90s and in New York, it almost makes me think, “Was it cheap to live in New York back then? Was the 90s just a wealthy time?” I guess until I invent a time machine, I will never know…

Technology has become so integrated in our day to day lives, I believe it has totally changed the way I do business. Not only this, but it has also helped my clients in gaining more knowledge and confidence in what they are investing in. This in turn, has helped me in my business, as I believe that knowledge is key to success. I am a Personal Wealth Manager who specialises in bespoke financial planning for clients in Singapore, blending personal and professional financial advice with all-important tax planning. I wanted to share with everyone that platforms and tools I currently use to help my clients, plus some tools that the everyday investor can use to successfully plan, visualise and research your investments and finances.

FE Analytics

This online platform is a complete game-changer for me. FE Analytics is more worthwhile for financial planners, investment analysts and others in the finance space, because the subscription fee is quite substantial, but it is an invaluable tool. I use it to create portfolios for clients, review and project investments and compare their current portfolios with bespoke ones I have created for them. What I love about this platform is that it will gather global data, from companies like Bloomberg, Yahoo Finance and others of the sort, to compare key investment data points, such as performance vs. benchmark, volatility, risk and even ESG rating. Volatility and risk are an excellent thing to show to clients, as they can clearly see how erratic their investments are in comparison to their performance. In today’s ever-changing world, many of my clients are become more conscientious and circular economy-focused, so being able to show an ESG rating adds value to them.

Even though an average investor may not have access to this platform, it is important to know that every legitimate investment will have a code, which can and should be easily found on websites, such as Yahoo Finance, so that you can clearly see the funds performance, fees and charges, and have full transparency in information of the investment. If you cannot find this number, or there is no information online about your investment, this could be a red flag.

OPAL Fintech

OPAL is one digital business account for your business and financial needs. I really enjoy using this platform because it is a perfect visualisation of a person’s goals, dreams, aspirations and current situation. All I have to do is input a client’s cash flow, assets, debt, and then discuss with them their financial goals. This may be plans for retirement, saving for a property, planning for a child’s education, or even leaving a lumpsum for their family when they pass on. The OPAL algorithm will assess their current situation, factor is real-life data, such as inflation, and project how likely it is for that goal to happen. Then, it can be tweaked and adjusted, showing multiple scenarios depending on how much the client is setting aside into investments. I often feel like, because financial planning is very numbers-heavy, people can find it difficult to visualise their goals clearly. I don’t have that issue with OPAL, because the graphics and projections perfectly paint the picture for the client.

Budgeting Platforms

But what if you do not have access to these paid platforms? I would first off recommend tracking your cashflow on a monthly basis and being conscious of your assets vs. debts. There are loads of budgeting apps that you can use. For example, DBS Online Banking has an interface that illustrates your monthly inflowing cash and outgoings. If you’d like something a bit more in depth, so that you can go through these figures with a find-toothed comb, I would recommend apps like Zenmoney, Monny or Spendee; all of these (and ones similar) are free and user-friendly for the consumer. Some will consolidate your spending habits into presentable data and graphics, others will incorporate some gamification in order to encourage you to hit your spending and saving goals. There are many on the market in Singapore, and you just have to play around and find whatever works for you. I prefer to use the DBS NAV Planner paired with an Excel spreadsheet, but others may prefer the other apps mentioned here.

Stock Screener

If you are investing in individual stocks, or if your portfolio comprises of equities, you can always use stock screeners to check key analytics like the market cap, yield and sector. You can also delve further into the figures and statistics, like viewing the past 5 years performance and other metrics. You can also check company announcements and financial statements, which is perfect for those investors that like to research in depth. For Singapore stock exchange, you can use https://investors.sgx.com/stock-screener.

General Learning & Boosting Your Knowledge

As I mentioned at the start of my article, knowledge is power. If you don’t have a basic level of knowledge, this is quite often the blockade that is stopping you from investing, which means that your money is being eroded by inflation. You may be concerned of misinformation out there, but don’t worry, there are many great, informative platforms you can use to educate yourself. The first is Investopedia, which is essentially a Wikipedia for all things money and investing. Here you can find simple to understand financial concepts, investment terms and even information on past historical events in the finance world. The Balance is a great website that hosts a wide range of information, from which loans give the best rates, what stock market apps are easy to use, to how to discuss finances with your children. This is really a font of knowledge and a go-to for anyone who just wants to get more clued up on finance. I would of course recommend keeping yourself up-to-date with news by checking out The Financial Times, Bloomberg and CNBC, as well as other credible finance media outlets.

In this world of technology, finance and investing have become accessible to the masses; what once seemed only for the super-savvy or wealthy, is now at the click of a button to almost everyone who owns a computer or smartphone. This readily available information is not something we should shy away from; these are wonderful tools we can use to do our own due diligence and ensure that we are planning our finances and investments correctly. Technology has pushed for a need for transparency in the finance sector, so what a better time to start investing! You have all the knowledge, resources and tools to do so responsibly, and with some level of understanding. However, for those that are not as savvy, or for those that have a full schedule, you may not have the time to commit to constant research. I don’t blame you- if it wasn’t my full-time job I probably wouldn’t either! This is when you can lean on the advice of a professional, who will have all these tools at their disposal, with the added expertise and wisdom to help you navigate investing effectively in accordance with your risk tolerance and unique circumstances.

(Remember that if you are struggling to find information available online of an investment, to tread lightly, as a lack of transparency may also mean a lack of legitimacy.)

You may have heard the word ‘volatility’ when referring to investments. When an investment, or market, is volatile, it means that there are great fluctuations and market disruptions. You may look at your investment one day, and it could be up by 20%, the next it may have dropped to -5%. Usually, if you hold your investment long-term, it will weather the short-term volatility, meaning that all of these ups and downs don’t matter too much, because your investment will have grown overall. A volatile investment can be a stressful one if you haven’t taken emotion out of investing. It’s always best to remember your investment goals, understand that investments work well long-term, and understand that the market will bounce back. If you haven’t read my article on ‘How To Take Emotion Out Of Investing’, you can read it here:

https://danielleteboul.com/2021/05/27/how-to-take-emotion-out-of-investing/: Is Volatility A Good Thing?Whilst volatility is inevitable- and investments with low fluctuations are generally more conservative and may not bring as high returns- is it a good thing for us as investors? Is the possible stress of a roller-coaster market worth it? What if I invest a lump sum at the wrong time? In this article, I will deep-dive into the question…is volatility a good thing?

No-one can successfully time the market correctly every single time, especially a novice investor who has a full time job and other responsibilities, meaning they can’t sit and watch the stock market all day. Therefore, I think it’s key to remember, ‘time in the market, versus timing the market’; drip feeding smaller amounts of money over regular intervals over the long term, can often mitigate the risk of volatility. This concept of ‘dollar-cost averaging’ is a very simple yet important strategy to remember. So long as you stay the same with your investments and don’t fluctuate on your stance, you can weather the ups and downs of the market.

As I hinted to earlier, an investment that barely fluctuates, is often more conservative in its risk profile, meaning that there may be lower risk of losses, but also the returns may not be high. On the flip side, a well chosen investment that fluctuates, may mean that your investment is volatile, but on the whole rises faster. So ask yourself, would you rather have little fluctuations in your investment and possibly never reach a decent rate of return, or would you be OK with taking the risk on the volatile investment in order to access to possible higher returns?

For those that are a bit more savvy, they may be keen to buy more at a dip in the market. Although timing the market is very difficult, sometimes the market will be down for a longer period of time. For example, the dot come bubble started collapsing in 1999 and didn’t end until 2002. Can you imagine how happy you would be if you had bought Apple or Microsoft stocks during this period, when the world was losing faith in new technology, and you had held onto those stocks until now? This is a brilliant example of being a market opportunist, whilst still having long-term investment goals. This is an extreme example, but the idea still stands. If the down period of the market has been continuous for quite some time, it’s best not to hesitate. If you have the capacity to invest more, do so before the market goes up, and reap the benefits in the future.

If you are struggling with emotionally dealing with market volatility, you may want to consider a hands off approach and engaging professionals to do the work for you. Fund managers will be able to understand the peaks and troughs of the funds, making well-informed and educated decisions on how to rebalance your portfolio. One of the strategies they will take will be diversification, essentially not having all your eggs in one basket. If you have a portfolio of a wide-range of investments in different asset classes and geographical locations, you mitigate the risk of losing it all if something goes wrong.

For example, imagine two people have invested in the Brazilian stock market; Person A has invested 80% of their portfolio, whilst Person B has only invested 5%, whilst having a basket of stocks in other areas. Now imagine that Brazil goes into political unrest, a military coup is held, and the new leader is isolationist…the Brazilian stock market busts! Oh no! Person A has lost 80% of their investment, and who knows how much it could drop, and maybe keep dropping! Whereas Person B has only lost 5% of his portfolio. Yes, this is annoying, but not as catastrophic as Person A’s situation. And who knows, Person B may have benefited in other areas. Maybe because of the situation in Brazil, the country no longer exports raw sugar, and this causes India’s raw sugar exports to go up. This is great news for Person B, because they have also invested in Indian funds, that have benefitted from the Brazilian coup!

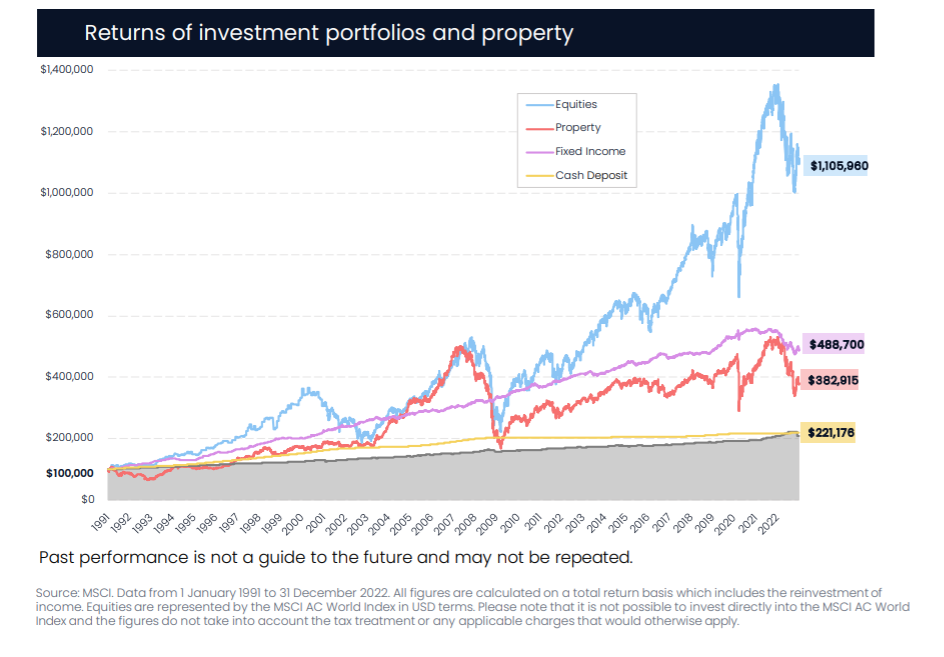

Whilst volatility often holds negative connotations, it is dangerous to think of it in this way. Volatility can work to our advantage, and be beneficial for us, so long as we stick to certain investment principles, such as dollar-cost averaging, taking the emotion out of investing and diversification. Not only that, if we are opportunistic about our lump sum investing, this could massively benefit us long term. As always, the key is that long-term investment strategies will be able to survive short-term market fluctuations. Here is an excellent diagram I found to demonstrate this. I hope you found this article useful, and if you did have any more questions on this topic, I would be happy to answer.

This chart shows the span between the largest average 1-year, 5-year, 10-year, and 20-year gains and losses among three key market indexes for the period 1926–2009. As you can see, short-term holdings (especially in stocks) are extremely volatile. Historically, a long-term approach has provided a much smoother ride.